+971 52 248 8528

+971 52 248 8528

+966 56 233 0183

+966 56 233 0183

In today’s interconnected world, businesses in Saudi Arabia frequently engage with foreign suppliers, service providers, and contractors. However, many companies may not be fully aware of the tax implications when making payments to non-residents. Withholding Tax (WHT) is one such requirement that can significantly affect cross-border transactions.

This comprehensive guide provides a detailed breakdown of tax on payments against invoices from outside Saudi Arabia. Whether you’re running a business in the Kingdom or managing international payments, understanding the tax system is crucial to ensure compliance and avoid unnecessary penalties.

What is Withholding Tax?

Withholding tax is a tax deducted at source from payments made by a Saudi resident entity (or permanent establishment) to a non-resident (foreign entity). It applies to payments for services, royalties, dividends, interest, and other income sources that arise from Saudi Arabia. Since foreign companies do not typically pay taxes directly in Saudi Arabia, the government collects this tax through the payer (the Saudi company), ensuring that foreign entities contribute to the national tax revenue for income earned from Saudi sources. Withholding Tax (WHT)

Key Terms and Definitions

- Withholding Tax (WHT): A tax deducted at the source of payment to non-residents.

- Non-Resident: A foreign company or individual that earns income from Saudi Arabia without a permanent establishment in the Kingdom.

- Resident Payer: The Saudi entity or permanent establishment making the payment to the non-resident.

When is Withholding Tax Applicable?

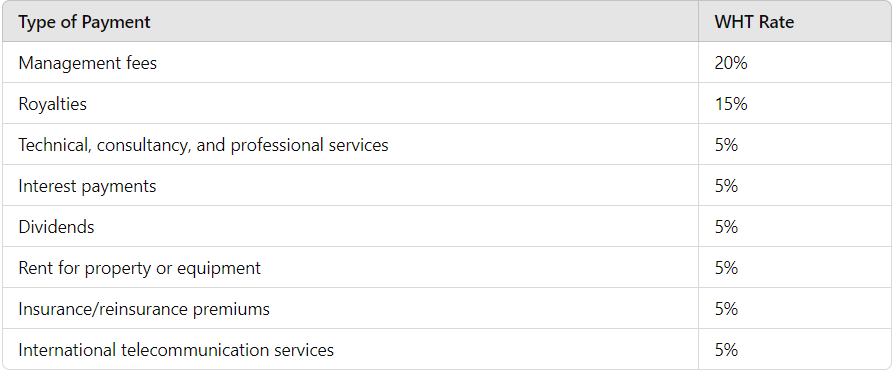

Tax is applicable whenever a Saudi company or a permanent establishment makes payments to a foreign entity for the following types of income:

- Service fees (e.g., consultancy, technical, or management services)

- Royalties (e.g., intellectual property usage, licenses)

- Interest payments (e.g., loans or financing)

- Dividends (profits paid to foreign shareholders)

- Rent (for equipment or real estate)

- International telecommunication services

Tax Rates in Saudi Arabia

The rates of withholding tax vary based on the nature of the payment being made. Below is a summary of the applicable rates for different types of payments:

It is important to note that Double Taxation Treaties (DTTs) may reduce or eliminate withholding tax rates for certain types of payments. Saudi Arabia has treaties with numerous countries, and businesses can benefit from reduced tax rates by providing the necessary documentation (e.g., tax residency certificates).

Example of Withholding Tax Calculation

Consider a Saudi company paying SAR 200,000 to a foreign consultancy service provider. The withholding tax rate for consultancy services is 5%.

Total Payment: SAR 200,000

Tax Rate: 5%

Tax Deducted: SAR 200,000 × 5% = SAR 10,000

In this example, the Saudi company will pay SAR 10,000 to ZATCA as withholding tax and transfer SAR 190,000 to the foreign consultancy provider.

How to File Withholding Tax in Saudi Arabia

- Registration: Ensure the Saudi entity is registered with the Zakat, Tax, and Customs Authority (ZATCA) to file withholding tax.

- Filing Process: The withholding tax return must be filed by the payer on or before the 10th day of the month following the payment to the non-resident.

- Payment to ZATCA: The withheld amount must be paid to ZATCA by the same deadline (before the 10th day of the next month).

- Tax Certificate: Upon successful payment, the Saudi company can request a Withholding Tax Certificate, which may help the foreign company avoid double taxation in its home country.

Double Taxation Treaties (DTTs)

Saudi Arabia has entered into Double Taxation Agreements (DTAs) with many countries to ensure that income is not taxed twice, both in Saudi Arabia and the recipient’s home country. These treaties can reduce the withholding tax rate or provide exemptions for certain types of income.

To benefit from DTTs, the non-resident (foreign entity) must provide the following:

- A tax residency certificate issued by their home country’s tax authority.

- Any other required documents as per the DTT rules.

Grossing-Up Payments: Ensuring Full Payment to the Non-Resident

In some cases, the contract between the Saudi entity and the foreign company may specify that the foreign entity should receive the full agreed amount without deductions for withholding tax. In this situation, the Saudi entity may need to gross up the payment.

For example, if a Saudi company agrees to pay a foreign supplier SAR 100,000 after tax, and the withholding tax rate is 5%, the gross payment required would be SAR 105,263. The Saudi entity would withhold SAR 5,263 as tax, ensuring that the foreign entity receives the full SAR 100,000 after tax.

Penalties for Non-Compliance

Failure to comply with withholding tax requirements can lead to significant penalties:

Late Payment Penalty: Ranges from 1% to 5% of the unpaid tax for each month the payment is delayed.

Filing Penalties: Penalties may also apply for late filing of the withholding tax declaration.

To avoid these penalties, it is crucial for businesses to ensure timely deduction, filing, and payment of withholding tax to ZATCA.

Practical Tips for Managing Withholding Tax

Review Contracts: Ensure that your contracts with foreign suppliers clearly specify whether withholding tax is included in the payment or must be deducted.

Keep Accurate Records: Maintain records of all payments made to non-residents and the taxes withheld to ensure accurate reporting to ZATCA.

Seek Professional Advice: Withholding tax regulations can be complex, especially when dealing with double taxation treaties. It is advisable to consult with tax professionals, such as J K Management Consultancies, for expert guidance and compliance solutions.

Conclusion

Withholding tax is a crucial part of the Saudi tax system, especially for companies dealing with foreign entities. Understanding when and how it applies, along with ensuring timely compliance, can help businesses avoid unnecessary penalties and build strong relationships with international partners.

For more information or assistance with tax compliance, business setup, or cross-border transactions, reach out to J K Management Consultancies, your trusted partner for tax, legal, and business advisory services in the Kingdom of Saudi Arabia.